2020 State of the Health Funds Report

Relating to the financial year 2019–20

Report required by s 20D(c) of the Ombudsman Act 1976.

All material presented in this publication is provided under a Creative Commons Attribution 3.0 Australia licence (creativecommons.org/licences).

This material may be copied, distributed, transmitted or adapted (including for commercial purposes) provided the Office of the Commonwealth Ombudsman is credited as the creator and is not represented as endorsing your use of the material.

To avoid doubt, this licence only applies to the material as set out in this document.

The details of the relevant licence conditions are available on the Creative Commons website, as is the full legal code for the CC BY 3.0 AU licence (creativecommons.org/licences/by/3.0/au).

Under the Coat of Arms—the terms under which the Australian Coat of Arms may be used are detailed on the It's an Honour website (itsanhonour.gov.au).

Foreword

I am pleased to present the 16th annual State of the Health Funds Report, relating to the financial year 2019–20. The Ombudsman Act 1976 requires that the Private Health Insurance Ombudsman (PHIO) publish the report after the end of each financial year to provide comparative information on the performance and service delivery of all health funds[1] during that financial year.

The information in the report supplements information available on our consumer website privatehealth.gov.au. The consumer website provides a range of information to assist consumers to understand private health insurance and to select or update their private health insurance policies. The information on the consumer website, together with the State of the Health Funds Report itself, makes it easier for consumers to choose health insurance policies that better meet their individual needs.

The purpose of this report is to provide consumers with additional information to assist them to make decisions about private health insurance. For existing policyholders, the report details information that allows them to compare the performance of their fund with all other health funds. For those considering taking out private health insurance for the first time, the report provides an indication of the services available from each fund and a comparison of some service and performance indicators at the fund level.

The range of issues and performance information contained in the report has been chosen after taking into account the availability of reliable data and whether the information is reasonably comparable across funds. The information included in the report is based on data collected by the Australian Prudential Regulation Authority (APRA), as part of its role in undertaking statistical reporting and monitoring of the financial management of health funds. I would like to thank APRA for their assistance and advice in relation to the preparation of this report.

![]()

Mr Michael Manthorpe PSM

Commonwealth Ombudsman

February 2021

Using this report to compare funds

Disclaimer:

- Nothing contained in this report should be taken as a recommendation by this Office in favour of any particular health fund or health insurance policy.

- No single indicator should be used as an indicator of overall fund performance.

- The information used in this report to compare health funds is based on data collected for regulatory purposes. This information is the most appropriate, independent and reliable data available at 1 December 2020.

- This report is intended to help consumers decide which health funds to consider, though it won't indicate which of the fund's policies to purchase. Most funds offer more expensive policies that can be expected to provide better than average benefits, as well as cheaper policies that provide less benefits.

The State of the Health Funds Report

The State of the Health Funds Report (SOHFR) compares how health funds perform across the following criteria:

- service performance

- hospital benefits

- medical gap schemes

- general treatment (extras) benefits

- financial management

- health fund operations.

Consumers can use the information contained in this report to identify funds to join or assess their current fund's performance relative to other funds.

The range of indicators included in this report allow consumers to focus on factors of most importance to them—not all factors will be of equal importance to every individual or family. For example, if a consumer prefers to do business with a health fund in person, then the availability of retail offices would be an important consideration. However, if they prefer to do the majority of their business online, the range of services available through the funds' websites will be more important.

More information about particular indicators is provided in the explanations preceding each of the tables in this report.

If a consumer is considering taking out private health insurance for the first time, we suggest they use the report to identify a number of funds—preferably at least three for further consideration.

Where to find more information about selecting a policy

The Ombudsman’s consumer website privatehealth.gov.au includes advice on what factors to consider and what questions to ask when selecting a policy. It also includes information on government incentives relating to hospital cover such as the 'Medicare Levy Surcharge Exemption' and 'Lifetime Health Cover'.

This report does not include detailed information on price and benefits for health insurance policies. Information on specific policies is available from privatehealth.gov.au, where you can search for and compare information about every health fund and policy in Australia.

Further information, brochures and factsheets on private health insurance can be found at ombudsman.gov.au. Some brochures can also be obtained in hard copy on request to the Ombudsman's Office.

Fund names

In this report, health funds are referred to by an abbreviation of their registered name, rather than any brand name they might use. This abbreviated name appears on the left side of the heading for each fund in the Health Fund Listing section. Some funds use several different brand names or have used brand names in the recent past:

Brand name | Fund |

|---|---|

AAMI | NIB |

APIA | NIB |

Astute Simplicity Health | St Lukes |

Australian Health Management | Medibank |

Budget Direct | GMHBA |

Emergency Services Health | Police Health |

Frank | GMHBA |

GMF Health | HBF |

GU Corporate Health | NIB |

Healthguard | HBF |

Hunter Health Insurance | CDH |

iSelf | Phoenix |

Kogan | Medibank |

Manchester Unity | HCF |

MyOwn Health | AIA Health |

NRMA Health | BUPA |

Qantas Assure | NIB |

Suncorp | NIB |

Territory Health | QCH |

UniHealth | Teachers Health |

Union Health | TUH |

About the data used in this report

Open and restricted membership health funds

Membership of 'open' health funds is available to everyone.

'Restricted membership' health funds have certain membership criteria which mean they are not available to all consumers. For example, membership may be restricted to employees of certain companies, occupations or members of particular organisations.

Where applicable, open and restricted membership funds are listed separately in each of the tables in this report.

Information about policies

The information included in this report on fund contributions and benefits indicates the average outcomes across all of a fund's policies, so this cannot be taken as an indicator of the price or benefit levels that can be expected for any particular policy.

Data collection

The majority of data selected by the Ombudsman as the most appropriate available, is collected by the industry regulator APRA. While funds report to APRA for regulatory purposes, some of this information is useful to consumers and is reproduced in this report. As this data is collected primarily for regulatory purposes, it is important to read the accompanying text explaining the data in conjunction with the tables.

As funds differ in size, most of the statistical information is presented as percentages or dollar amounts per membership, for easier comparison. No attempt has been made to weigh the importance of various indicators, as these are subjective judgements, dependent on the consumer’s individual circumstances, preferences and priorities. For this reason, it would not be valid to average all the scores indicated to obtain a form of consolidated performance or service delivery score.

The report provides consumers with additional information about the benefits that were paid by each fund over the last year. The report also provides information about the extent of cover provided for hospital, medical and general treatment, and any state-based differences in coverage. The selection of indicators used in this report is not intended to represent the full range of factors that should be considered when comparing the performance of health funds. The range of indicators has been limited to those for which there is reliable comparative information available.

Key consumer issues

Overview of complaints in 2020–21

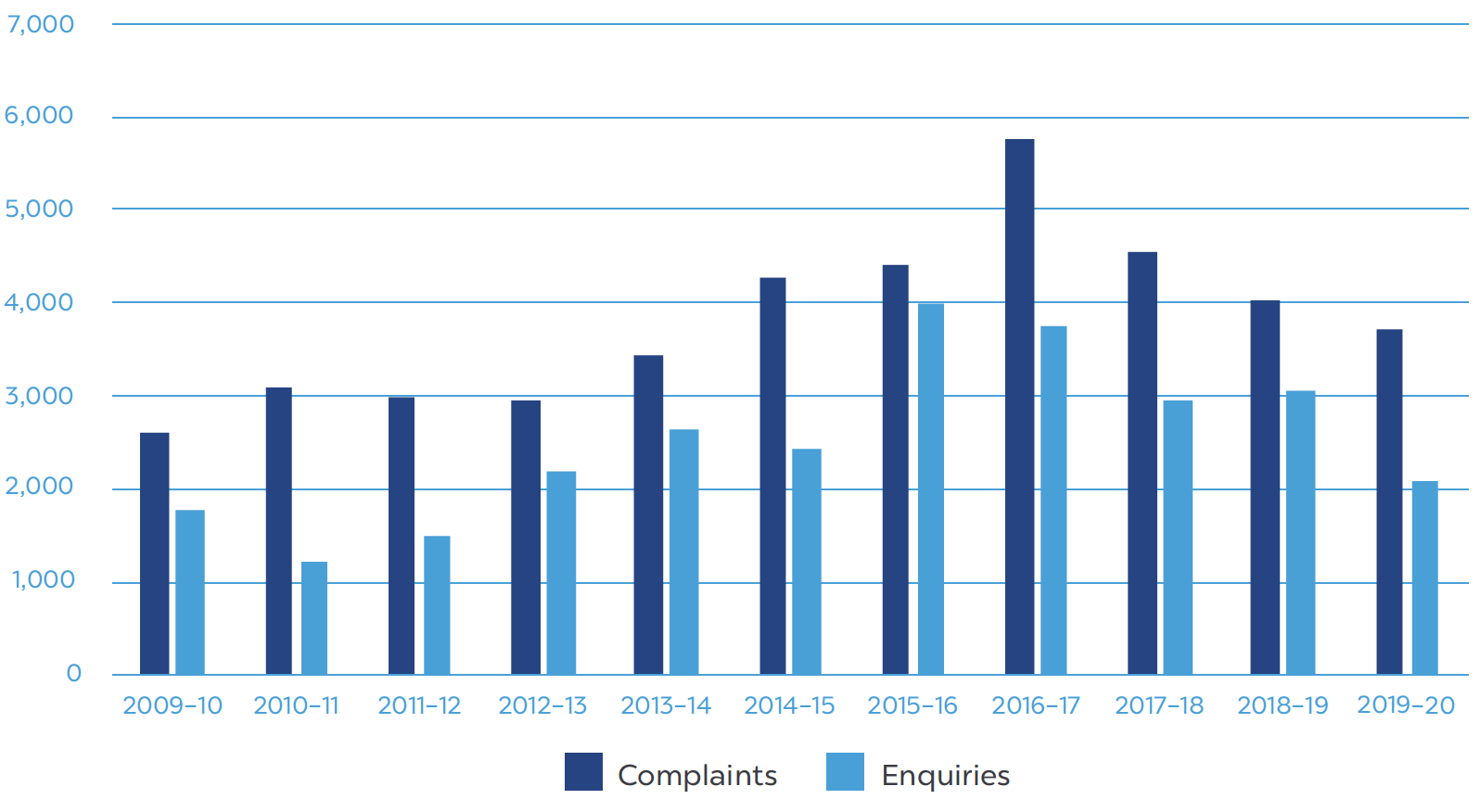

In 2019–20, the Office received 3,706 complaints about private health insurance, representing an 8.3 per cent decrease in complaints received compared to 2018–19. In the same period we also received 2,049 private health insurance enquiries.[2]

Figure 1—Total complaints and enquiries by year

Complaints

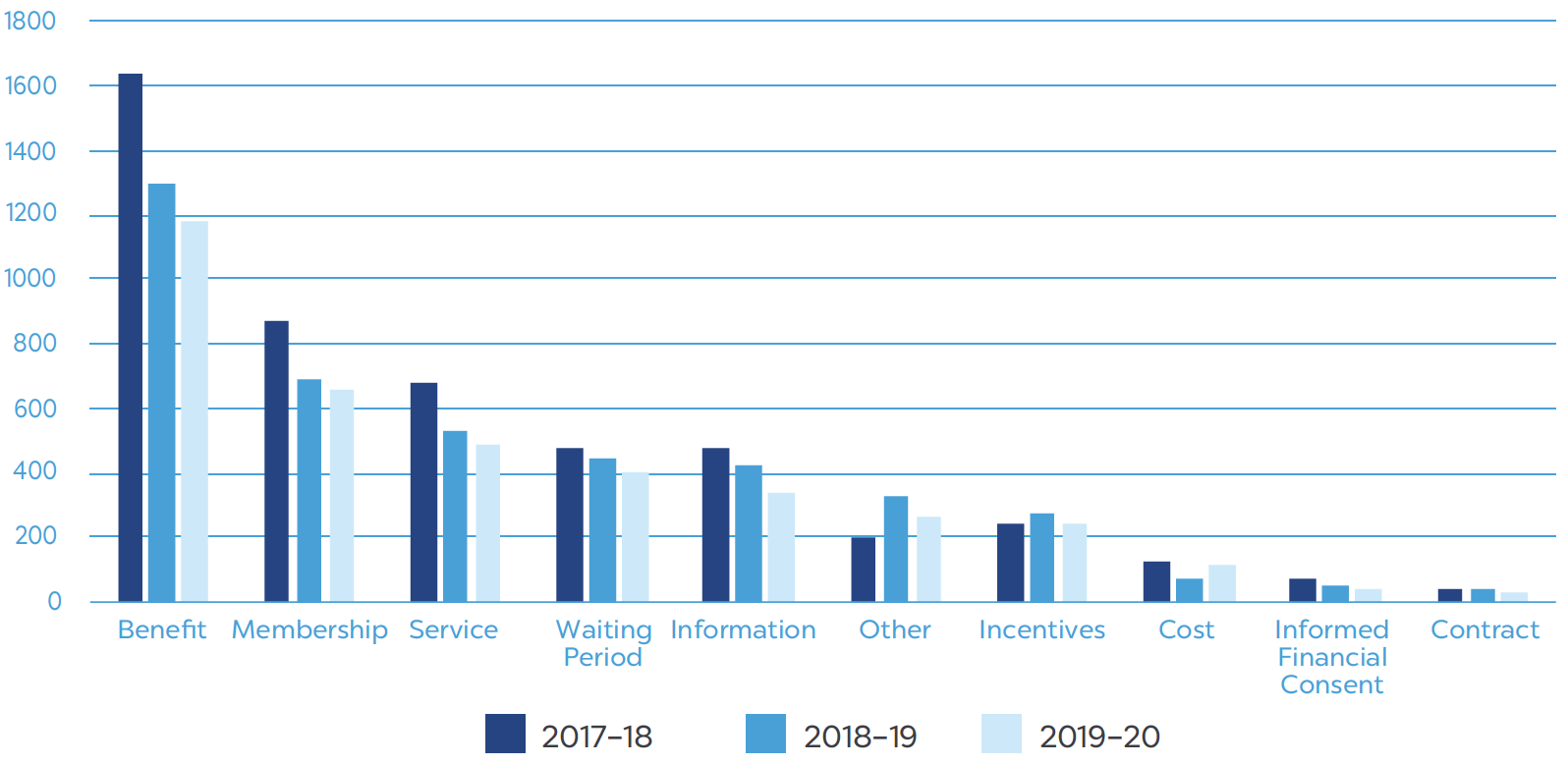

Concerns about benefits, membership and service continued to be the major cause of complaints to our Office.

The most significant benefit complaint issues were general treatment (extras/ancillary) benefits, and complaints about unexpected hospital policy exclusions and restrictions.

General treatment complaints usually concern disputes over the amount payable under ‘extras’ policies such as dental, optical, physiotherapy and pharmaceuticals, or the insurer’s rules for benefit payments (such as certain minimum claim criteria).

Some basic and budget levels of hospital cover exclude or restrict services that many consumers assume are routine treatments or standard items.

Complaints about delays in benefit payments also represented a significant proportion of complaints received, as did complaints about hospital and medical ‘gaps’ that resulted in an out of pocket expense to patients.

Membership complaints typically involved policy administration issues, such as the processing of cancellations or payment of premium arrears. Delays in the provision of transfer (also known as clearance) certificates when transferring between health insurers was also a significant cause of complaints. This year there was a significant increase in the number of complaints about membership suspensions due to COVID-19—this is discussed in further detail below.

Service issues are usually not the sole reason for complaints and a service failure is often just part of a complaint made to our Office. The combination of unsatisfactory customer service, delays in responding to simple issues and poor internal escalation processes can cause policyholders to become more aggrieved and dissatisfied with the insurer.

Figure 2—Complaint issues over previous three years

COVID-19 complaints

In the February to June 2020 period, the Office received 212 complaints and 43 enquiries related to COVID-19. The majority of these complaints raised issues related to suspension requests, premium costs and the inability to access hospital and general treatment services as planned.

The issue which caused the most COVID-19 complaints was membership suspension (62 complaints) where consumers sought temporary suspensions of membership due to financial hardship.

Almost all insurers postponed their 1 April 2020 premium increases for at least six months to 1 October 2020. The majority of insurers also introduced provisions to provide financial relief to people who have lost their jobs, are underemployed, in hardship or have contracted the virus; and most insurers covered COVID-19 treatment for existing policyholders.

Enquiries

The majority of enquiries received by our Office are general queries about how private health insurance works and Lifetime Health Cover (LHC). Thirty-three per cent of enquiries in 2019–20 fell into the category of private health insurance queries, including queries about what factors consumers should consider when selecting a policy.

Thirty per cent of enquiries were about Lifetime Health Cover (LHC). LHC is a set of rules which determines what an individual pays for private hospital insurance. Generally, if a person purchases hospital cover earlier in life and maintains cover, they will avoid paying an extra amount called 'LHC loading'. Some exemptions can apply for new Australian residents and Australians who have been living overseas. We experience an increase in contacts about LHC in the May to June period each year, as the deadline to take up private hospital insurance without incurring an extra LHC loading for most individuals is 30 June.

Consumers also contacted our Office to seek information about government incentives such as the government rebate and Medicare levy surcharge, health insurance for overseas visitors to Australia, the role of the Ombudsman and general advice about Australia’s healthcare system.

Some contacts received via our consumer website privatehealth.gov.au also provided feedback about website content and the tools available to consumers, such as the policy search feature and the LHC calculators.

Consumer website privatehealth.gov.au

The website privatehealth.gov.au is Australia’s leading independent source of consumer information about private health insurance. It is also the only website that allows users to search the features and premium costs of every policy available in Australia.

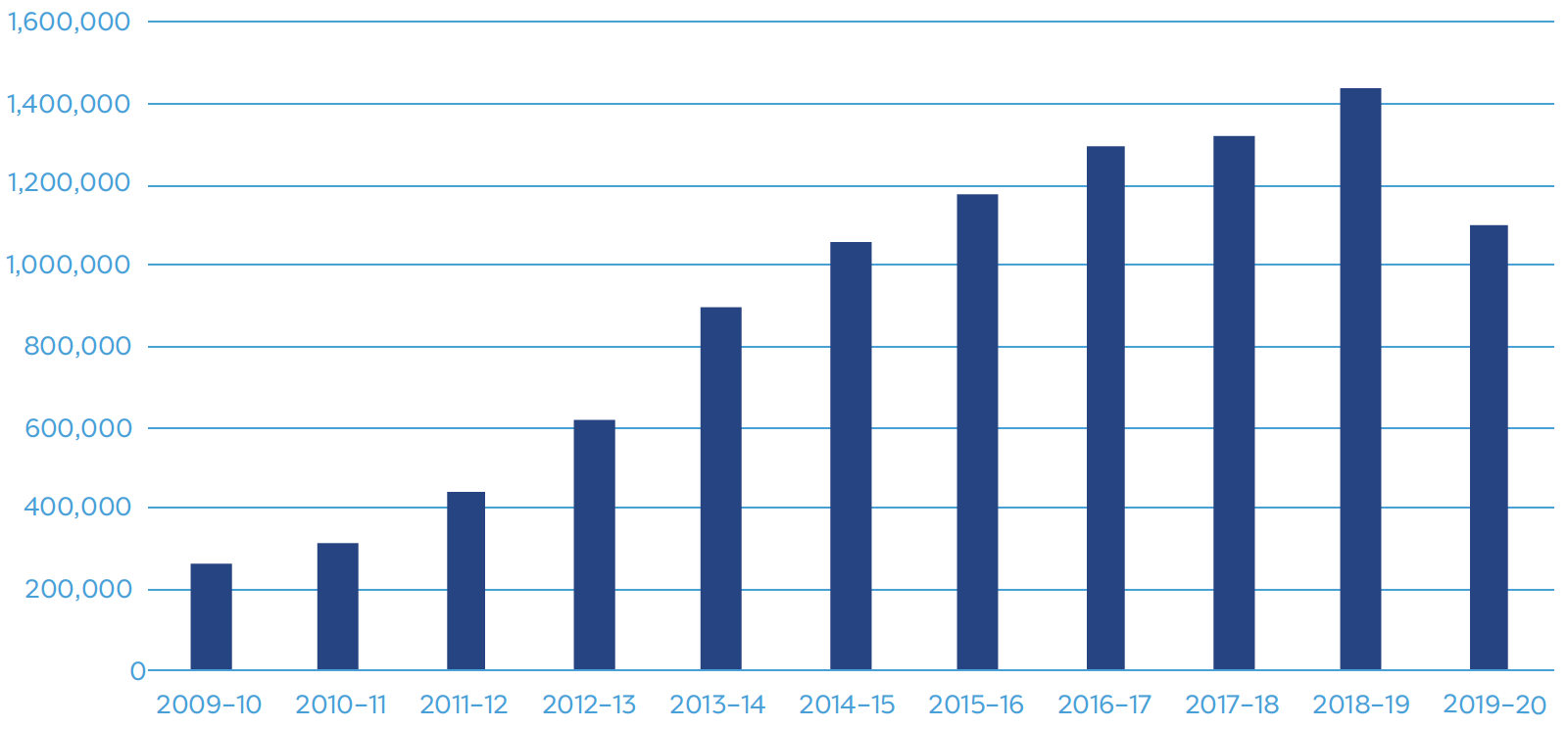

In 2019–20 we received 1,270 enquiries via the consumer website, which we responded to with information and advice.

Website usage decreased in 2019–20, with 1,098,631 visitors compared to 1,441,712 visits in 2018–19. This is partially a result of the Office’s decision to publish Private Health Information Statement (PHIS) data on data.gov.au, with some visitors now sourcing their information from this secondary source. The website continues to rely on organic growth, with the majority of visitors discovering the website through search engines.

Figure 3—privatehealth.gov.au visitors per year

Health fund listing and contact details

The following table lists all Australian registered health funds. The 'open' membership funds provide policies to the general public. The 'restricted' funds provide policies through specific employment groups, professional associations or unions.

| Open Membership Health Funds | |||

|---|---|---|---|

| Abbreviation | Full name or other names | Phone Number | Website |

| AIA Health | AIA Health Insurance, MyOwn Health Insurance | 1800 333 004 | www.aia.com.au/health |

| Australian Unity | Australian Unity Health Ltd | 132 939 | australianunity.com.au |

| BUPA | Bupa HI Pty Ltd | 134 135 | bupa.com.au |

| CBHS Corporate | CBHS Corporate Health Pty Ltd | 1300 586 462 | cbhscorporatehealth.com.au |

| CDH | CDH – Hunter Health Insurance | 02 4990 1385 | hunterhi.com.au |

| CUA Health | CUA Health Ltd | 1300 499 260 | cua.com.au/health-insurance |

| GMHBA | GMHBA Ltd, Frank | 1300 446 422 | gmhba.com.au |

| HBF | HBF Health Ltd | 133 423 | hbf.com.au |

| HCF | Hospitals Contribution Fund of Australia | 131 334 | hcf.com.au |

| HCI | Health Care Insurance Ltd | 1800 804 950 | hciltd.com.au |

| Health.com.au | Health.com.au | 1300 199 802 | health.com.au |

| Health Partners | Health Partners Ltd | 1300 113 113 | healthpartners.com.au |

| HIF | Health Insurance Fund of Australia Ltd | 1300 134 060 | hif.com.au |

| Latrobe | Latrobe Health Services | 1300 362 144 | latrobehealth.com.au |

| MDHF | Mildura Health Fund Ltd | 03 5023 0269 | mildurahealthfund.com.au |

| Medibank | Medibank Private Ltd, Australian Health Management | 132 331; 134 246 | medibank.com.au; ahm.com.au |

| NIB | NIB Health Funds Ltd, Qantas Assure, APIA | 131 463 | nib.com.au |

| Onemedifund | National Health Benefits Australia Pty Ltd | 1800 148 626 | onemedifund.com.au |

| Peoplecare | Peoplecare Health Insurance Limited | 1800 808 690 | peoplecare.com.au |

| Phoenix | Phoenix Health Fund Ltd | 1800 028 817 | phoenixhealthfund.com.au |

| QCH | Queensland Country Health Fund Ltd | 1800 813 415 | www.queenslandcountry.health |

| St Lukes | St. Lukes Health | 1300 651 988 | stlukes.com.au |

| Transport Health | Transport Health Pty Ltd | 1300 806 808 | transporthealth.com.au |

| Westfund | Westfund Limited | 1300 937 838 | westfund.com.au |

| Restricted membership health funds | |||

| Abbreviation | Full name or other names | Phone Number | Website |

| ACA | ACA Health Benefits Fund | 1300 368 390 | acahealth.com.au |

| CBHS | CBHS Health Fund Ltd | 1300 654 123 | cbhs.com.au |

| Defence Health | Defence Health Ltd | 1800 335 425 | defencehealth.com.au |

| Doctors' Health | The Doctors' Health Fund | 1800 226 126 | doctorshealthfund.com.au |

| Navy | Navy Health Ltd | 1300 306 289 | navyhealth.com.au |

| Nurses and Midwives | Nurses and Midwives Health Pty Ltd | 1300 344 000 | nmhealth.com.au |

| Police Health | Police Health Limited | 1800 603 603 | policehealth.com.au |

| Reserve Bank | Reserve Bank Health Society Ltd | 1800 027 299 | myrbhs.com.au |

| RT Health Fund | Railway and Transport Health Fund Ltd | 1300 886 123 | rthealthfund.com.au |

| Teachers Health | Teachers Federation Health Ltd | 1300 728 188 | teachershealth.com.au |

| TUH | Teachers' Union Health Fund | 1300 360 701 | www.tuh.com.au |

Service Performance

The level of complaints that we receive about a fund, relative to its market share, is a reasonable indicator of the service performance of most funds.

Whether a fund can attract new members and more importantly, retain members is also an indicator of member satisfaction.

Member retention

The member retention indicator is used as one measure of the comparative effectiveness of health funds and their level of member satisfaction. This indicator measures what percentage of fund members (hospital memberships only) have remained with the fund for two years or more.

This figure is calculated on the total gain or loss of members over the last two years, which takes into account consumers who take up membership and leave within that two year period. Figures are not adjusted for policies that lapse when a member dies, as these are not reported to APRA.

Most restricted membership funds rate well on this measure compared to open membership funds. This may be due to particular features of restricted membership funds, especially their links with employment.

Membership change

The membership change indicator shows the change in the number of policyholders over the year from 30 June 2019 to 30 June 2020. Both the percentage change and number are included. Negative figures indicate that the fund has experienced a net reduction in membership over the period. As indicated above, member deaths would contribute to this figure.

Ombudsman complaints in context

The number of complaints received by this Office is very small compared to fund membership.

There are a number of factors (other than service performance) that can influence the level of complaints we receive about a fund. These include the information provided to fund members about the Ombudsman through general publicity or by the fund and the effectiveness of the fund's own complaint handling process.

Complaints percentage compared to market share percentage

| Fund name (Abbreviated) | Member retention (hospital cover) [1] | Membership change % (number) [2] | Market share | Complaints % compared to market share % | Code of conduct member | |||

|---|---|---|---|---|---|---|---|---|

| Benefits | Service | All complaints | Complaints investigated | |||||

| Open membership funds | ||||||||

| Australian Unity | 78% | -4.9% (-8,791) | 2.6% | 3.7% | 5.3% | 4.5% | 1.8% | Yes |

| BUPA | 84% | -0.8% (-13,816) | 25.4% | 18.7% | 21.5% | 21.5% | 27.9% | Yes |

| CUA Health | 79% | 1.1% (428) | 0.6% | 0.3% | 1.4% | 0.8% | 1.5% | Yes |

| GMHBA | 71% | -8.9% (-13,864) | 2.1% | 3.8% | 2.4% | 3.3% | 2.9% | Yes |

| HBF | 86% | -2.3% (-11,395) | 7.3% | 4.2% | 4.3% | 4.0% | 2.6% | Yes |

| HCF | 88% | 5.9% (43,636) | 11.7% | 17.0% | 13.8% | 16.4% | 17.6% | Yes |

| Health.com.au | 70% | -14.4% (-5,648) | 0.5% | 1.0% | 1.0% | 1.1% | 3.3% | No |

| Health Partners | 90% | 5.1% (2,254) | 0.7% | 0.7% | 0.7% | 0.7% | 0.4% | Yes |

| HIF | 71% | -5.8% (-3,120) | 0.8% | 1.3% | 0.7% | 1.8% | 2.9% | Yes |

| Latrobe | 76% | -1.7% (-728) | 0.6% | 0.9% | 0.2% | 0.7% | 0.4% | Yes |

| Medibank | 75% | 0.6% (10,560) | 26.9% | 23.4% | 27.4% | 22.8% | 16.5% | Yes |

| NIB | 78% | 1.9% (11,690) | 9.2% | 10.7% | 7.9% | 8.1% | 4.4% | Yes |

| Peoplecare | 80% | -2.8% (-961) | 0.5% | 0.4% | 0.2% | 0.5% | 0.7% | Yes |

| St Lukes | 86% | 5.5% (1,843) | 0.5% | 0.5% | 0.5% | 0.4% | 1.1% | Yes |

| Westfund | 85% | 8.3% (4,435) | 0.9% | 1.2% | 1.0% | 0.9% | 1.5% | Yes |

| Restricted membership funds | ||||||||

| CBHS | 91% | 0.6% (566) | 1.5% | 1.0% | 3.3% | 2.2% | 2.9% | Yes |

| Defence Health | 88% | 1.0% (1,370) | 2.1% | 2.1% | 1.4% | 1.8% | 1.8% | Yes |

| Teachers Health | 90% | 2.2% (3,632) | 2.5% | 3.0% | 1.2% | 2.4% | 1.8% | Yes |

| TUH | 84% | -9.8% (-301) | 0.6% | 0.4% | 0.0% | 0.2% | 0.0% | Yes |

| Fund Name (Abbreviated) | Member retention (hospital cover) | Membership change [1] % (number) | Number complaints Received | Below market share? | Number complaints investigated | Below market share? | Code of conduct member | |

|---|---|---|---|---|---|---|---|---|

| Open membership funds | ||||||||

| AIA Health | 52% | 10.1% (1,320) | 49 | No | 12 | No | No | |

| CBHS Corporate | 70% | -6.7% (-92) | 1 | Yes | 0 | Yes | Yes | |

| CDH | 85% | 6.9% (191) | 2 | Yes | 0 | Yes | No | |

| HCI | 83% | -6.0% (-374) | 4 | No | 0 | Yes | Yes | |

| MDHF | 91% | 3.1% (513) | 0 | Yes | 0 | Yes | No | |

| Onemedifund | 91% | 1.2% (69) | 0 | Yes | 0 | Yes | Yes | |

| Phoenix | 85% | 4.0% (373) | 6 | No | 0 | Yes | Yes | |

| QCH | 86% | 2.1% (569) | 3 | Yes | 0 | Yes | Yes | |

| Transport Health | 72% | -11.6% (-712) | 22 | No | 1 | No | Yes | |

| Restricted membership funds | ||||||||

| ACA | 91% | 0.3% (13) | 0 | Yes | 0 | Yes | Yes | |

| Doctors' Health | 90% | 8.8% (1,937) | 10 | Yes | 0 | Yes | Yes | |

| Navy Health | 86% | 4.0% (896) | 10 | No | 1 | Yes | Yes | |

| Nurses and Midwives | 68% | 18.5% (885) | 8 | No | 0 | Yes | No | |

| Police Health | 91% | 13.8% (3,212) | 10 | Yes | 0 | Yes | Yes | |

| Reserve Bank | 88% | -0.5% (-12) | 2 | No | 0 | Yes | Yes | |

| RT Health Fund | 86% | -4.3% (-1,077) | 13 | No | 3 | No | Yes | |

[1] The total gain or loss of members over the last two years, which takes into account consumers who take up membership and leave within that two year period.

[2] Membership change in total policies. The industry experienced a growth of 0.42 per cent or 28,193 memberships overall.

Note: 'N/A' indicates no data as the insurer commenced operations during the previous two years.

In that table each fund's market share (as at 30 June 2020) is shown in the market share column. Subsequent columns show the percentage of Ombudsman complaints in various categories, received about each fund. These percentages should be compared with the market share percentage. Where a fund had a higher complaints percentage than its market share, it indicated that members of that fund were more likely to complain than the average of all fund members.

The table also indicates what percentage of benefit and service complaints are received about each fund:

Benefit complaints include problems of non-payment, delayed payment, the level of benefit paid or the gap paid by the member.

Service complaints are about the general quality of service provided by fund staff, the quality of customer service advice and premium payment problems.

All complaints takes account of all complaints received by this Office about the fund. All complaints includes complaints investigated as well as complaints that were finalised without the need for investigation.

Complaints investigated is a measure of the percentage of complaints that required a higher level of intervention from the Ombudsman, in relation to all complaints investigated. Most complaints to the Ombudsman can be finalised by referring the matter to fund staff to resolve, or by Ombudsman staff providing information to the complainant. Complaints which fund staff have not been able to resolve to a member's satisfaction are investigated by the Ombudsman's Office—so the rating on complaints investigated is an indicator of the effectiveness of each fund's own internal complaint handling.

Smaller funds (less than 0.5 per cent national market share)

For funds with less than 0.5 per cent of the national market share, it is not practical to show the percentage of complaints in each of the above categories because of the very small numbers of complaints.

Table 2B shows the actual number of all complaints received and the number of complaints investigated, as well as whether the number is below the fund's market share.

While these funds have a very low national market share, many are still significant in a particular state or region.

Code of Conduct

The self-regulatory code of conduct for health funds deals with the quality of advice provided to consumers and sets standards for training of health fund staff and others responsible for advising consumers about private health insurance. It also requires funds to have effective complaint handling procedures. Funds that have completed the compliance processes for becoming a signatory to the code are indicated in the table.

For more information about the Code of Conduct, please see: privatehealthcareaustralia.org.au/codeofconduct/

Table 2A—Membership retention and complaints (greater than 0.5 per cent market share)

Table 2B—Smaller funds (less than 0.5 per cent national market share)

Private hospital treatment

Table 3 provides a general comparison of health insurance for private patient hospital treatment. A higher percentage indicates that, on average, the fund's members are covered for a higher proportion of private hospital charges.

It's important to remember most funds offer a choice of different policies—the percentages indicated in this table are not indicative of any single policy, but are an average of all policies offered by the fund.

Hospital policies

Hospital policies provide benefits towards the following costs if you elect to be a private patient in a private or public hospital:

- hospital fees for accommodation, operating theatre charges and other charges raised by the hospital

- the costs of drugs or prostheses required for hospital treatment

- fees charged by doctors (surgeons, anaesthetists, pathologists, etc.) for in-hospital treatment.

Most funds offer a range of different policies providing hospital cover. These policies may differ on the basis of the range of treatments that are covered, to what extent those treatments are covered, the level of excess or co-payments you may be required to pay if you go to hospital and the price and discounts available to you.

Table 3 indicates the proportion of total charges associated with treatment of private patients covered by each fund's benefits. This includes charges for hospital accommodation, theatre costs, prostheses and specialist fees (not including the Medicare benefit), excesses or co-payments and associated benefits.

The figures shown are average outcomes across all of each fund's hospital policies. Higher cost policies will generally cover a greater proportion of charges than indicated by this average. Cheaper policies, including those with higher excesses or co-payments, may cover less.

The use of an average figure applying across all of each fund's policies will mean that funds with a high proportion of their membership in lower cost/restricted and excluded benefit policies will have a lower average figure.

Information is not provided for some funds in some states, where there is no activity in that state reported to APRA—generally this occurs in states where the fund does not have a large membership.

Hospital related charges covered (per cent) is calculated as: (Hospital benefits paid by insurer / Fees excluding medicare benefit)*100.

‘Fees’ is equal to the total amount the patient would have to pay to the provider(s) in the absence of any private health insurance, inclusive of hospital, medical and prostheses fees. This amount excludes the Medicare benefit. The difference between fees charged and benefits paid is the amount that the patient has to pay (out of pocket).

Additional information

The separate Health fund operations by state or territory tables in this report includes information on the number of 'agreement hospitals' under contract to each fund in each state.

For additional information on the medical gap benefits provided through hospital policies, please refer to the separate Medical gap schemes section.

The privatehealth.gov.au website provides information about all private health insurance policies available in Australia, including benefits, prices and agreement hospitals for each health fund.

| Fund name (Abbreviated) | % Hospital related charges covered [1] | |||||||

|---|---|---|---|---|---|---|---|---|

| ACT | NSW | VIC | QLD | SA | WA | TAS | NT | |

| Open membership funds | ||||||||

| AIA Health | 73.4% | 85.1% | 86.8% | 88.1% | 88.0% | 86.3% | 86.4% | 83.5% |

| Australian Unity | 81.4% | 88.4% | 91.3% | 89.2% | 89.8% | 88.9% | 91.5% | 87.9% |

| BUPA | 84.3% | 90.1% | 93.4% | 91.6% | 95.2% | 89.7% | 93.9% | 91.7% |

| CBHS Corporate | 70.7% | 86.4% | 80.9% | 93.3% | 95.2% | 88.5% | 88.5% | N/A |

| CDH | 56.6% | 96.0% | 89.4% | 91.8% | 94.3% | 95.7% | 92.2% | N/A |

| CUA Health | 81.1% | 90.2% | 90.3% | 92.1% | 90.1% | 88.6% | 91.6% | 80.2% |

| GMHBA | 78.0% | 85.0% | 92.0% | 87.3% | 89.9% | 91.1% | 91.6% | 80.7% |

| HBF | 87.8% | 90.2% | 93.0% | 91.9% | 93.9% | 95.5% | 95.4% | 87.5% |

| HCF | 89.4% | 93.1% | 93.3% | 92.3% | 94.7% | 90.9% | 93.5% | 92.1% |

| HCI | 86.1% | 88.8% | 92.6% | 91.4% | 92.5% | 95.8% | 94.3% | N/A |

| Health.com.au | 74.3% | 81.6% | 83.1% | 83.6% | 87.1% | 85.7% | 85.6% | 88.0% |

| Health Partners | 83.3% | 91.4% | 91.1% | 93.1% | 95.4% | 89.7% | 90.4% | 84.4% |

| HIF | 82.0% | 88.7% | 91.3% | 90.8% | 91.4% | 92.5% | 94.8% | 84.1% |

| Latrobe | 82.7% | 90.9% | 92.2% | 90.3% | 94.5% | 93.8% | 91.9% | 92.4% |

| MDHF | 69.8% | 94.1% | 93.5% | 91.3% | 93.1% | 91.8% | 92.3% | 99.7% |

| Medibank | 84.3% | 90.1% | 92.7% | 90.7% | 93.1% | 90.7% | 93.7% | 90.9% |

| NIB | 78.4% | 87.9% | 86.3% | 84.6% | 90.9% | 86.7% | 90.5% | 81.6% |

| Onemedifund | 76.6% | 93.6% | 95.3% | 95.0% | 95.8% | 95.5% | 95.6% | N/A |

| Peoplecare | 82.3% | 92.3% | 93.3% | 91.4% | 94.4% | 94.1% | 94.1% | 86.5% |

| Phoenix | 90.1% | 94.1% | 92.2% | 93.3% | 96.7% | 92.0% | 97.6% | 84.9% |

| QCH | 76.4% | 93.2% | 92.2% | 89.2% | 78.7% | 92.9% | 93.6% | 90.1% |

| St Lukes | 84.9% | 92.3% | 91.1% | 91.4% | 94.7% | 93.0% | 93.8% | 84.2% |

| Transport Health | 55.6% | 85.9% | 94.1% | 89.8% | 88.6% | 85.3% | 99.2% | N/A |

| Westfund | 84.8% | 93.6% | 91.7% | 91.2% | 93.8% | 92.0% | 95.7% | 92.6% |

| Restricted membership funds | ||||||||

| ACA | 92.7% | 95.0% | 97.0% | 96.1% | 95.0% | 95.7% | 95.6% | N/A |

| CBHS | 86.6% | 90.7% | 94.0% | 92.8% | 95.4% | 92.7% | 93.9% | 96.2% |

| Defence Health | 84.8% | 90.0% | 92.9% | 91.7% | 94.3% | 92.1% | 92.2% | 90.6% |

| Doctors' Health | 91.5% | 92.6% | 93.6% | 93.2% | 92.1% | 88.5% | 90.2% | 89.0% |

| Navy Health | 83.7% | 91.3% | 92.4% | 91.3% | 94.1% | 94.3% | 93.5% | 92.4% |

| Nurses and Midwives | 83.4% | 92.0% | 90.7% | 90.8% | 92.8% | 91.6% | 93.4% | 93.7% |

| Police Health | 82.8% | 88.8% | 93.3% | 92.6% | 97.0% | 92.6% | 94.5% | 94.4% |

| Reserve Bank | 88.1% | 93.7% | 97.6% | 97.6% | 97.9% | 98.1% | 98.1% | 99.8% |

| RT Health Fund | 83.6% | 92.6% | 91.6% | 93.5% | 95.9% | 90.9% | 96.3% | 84.5% |

| Teachers Health | 86.6% | 92.3% | 92.9% | 92.9% | 94.3% | 92.3% | 94.6% | 89.4% |

| TUH | 90.6% | 91.1% | 89.5% | 92.4% | 93.8% | 93.0% | 95.0% | 90.3% |

| Industry average | 84.7% | 90.8% | 92.4% | 91.1% | 94.6% | 93.5% | 93.7% | 91.2% |

[1] Includes charges for hospital accommodation, theatre costs, prostheses and specialist fees (not including the Medicare benefit) and associated benefits (after any excesses and co-payments are deducted).

Note: 'N/A' signifies no activity in that state. 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

Medical gap schemes

Health insurer 'medical gap schemes' are designed to eliminate or reduce the out of pocket costs incurred by a patient for in-hospital medical services. If a service is 'no gap,' it means no cost was incurred by the patient, as the full cost was covered by Medicare and the health fund. A reduced cost is incurred by the patient for what is called a 'known gap' service.

If a health fund has a higher percentage of services covered at no gap than other funds, it indicates the fund has a more effective gap scheme in that state. The figures provided are averages—it is no guarantee that a particular doctor will choose to use the fund's gap scheme.

Fund gap schemes and agreements

Doctors are free to decide whether or not to use a particular fund's gap cover arrangements for each individual patient. Factors that can affect the acceptance of the scheme by doctors include:

- whether the fund has a substantial share of the health insurance market in a particular state or region

- the level of fund benefits paid under the gap arrangements (compared with the doctor's desired fee)

- the design of the fund's gap cover arrangements, including any administrative burden for the doctor.

State-based differences

Information is provided on a state basis because the effectiveness of some funds' gap schemes can differ between states and these differences are not apparent in the national figures.

Most differences are due to the level of doctors' fees, which vary significantly between different states, regional areas and capital cities. In some states, funds are able to provide more effective coverage of gaps because doctors charge less than the national average. In addition, where a doctor's fee for an in-hospital service is at or below the Medicare Benefits Schedule fee, there will be no gap to the fund member.

If a health fund's percentage of services with no gap is higher than that of a fund in another state, it does not necessarily mean the fund's scheme is more effective, because state-based differences could be the cause.

Information is not provided for some funds in some states, as the numbers are not reported to APRA for states in which the fund does not have a sufficiently large membership (in which case, these figures are included with figures for the state in which a fund has the largest number of members).

Comparing different gap schemes

If a health fund has a higher percentage of services covered at no gap (in the same state/territory) compared with another fund, it is an indicator of a more effective gap scheme in that state. Over the whole fund, it is more likely that a medical service can be provided at no cost to the consumer, but it is no guarantee that a particular doctor will choose to use the fund's gap scheme.

Percentage of services with no gaps—the proportion of services for which a gap is not payable by the patient after accounting for fund benefits, schemes and agreements.

Percentage of services with no gap or where known gap payment made—this table includes both the percentage of no gap services and what is called 'known gap' services. Known gap schemes are an arrangement where the fund pays an additional benefit on the understanding that the provider advises the patient of costs upfront.

These tables take into account all of the fund's policies. The information in the tables is not indicative of any individual policy offered by the fund but is an average for the total fund membership.

| Fund Name (Abbreviated) | % of Services with no gap | |||||||

|---|---|---|---|---|---|---|---|---|

| ACT | NSW | VIC | QLD | SA | WA | TAS | NT | |

| Open membership funds | ||||||||

| AIA Health | 73.9% | 84.9% | 86.8% | 87.7% | 85.8% | 83.0% | 78.7% | 72.2% |

| Australian Unity | 79.6% | 91.9% | 91.9% | 91.5% | 91.8% | 87.4% | 92.6% | 95.1% |

| BUPA | 85.0% | 92.0% | 93.0% | 94.3% | 94.2% | 88.8% | 93.4% | 91.3% |

| CBHS Corporate | 68.4% | 85.4% | 92.1% | 91.3% | 98.7% | 81.6% | 72.3% | N/A |

| CDH | 52.9% | 87.5% | 60.5% | 72.6% | 63.4% | 42.9% | 68.1% | N/A |

| CUA Health | 79.3% | 92.4% | 90.5% | 94.3% | 87.9% | 87.3% | 90.2% | 77.5% |

| GMHBA | 55.0% | 78.0% | 86.9% | 81.9% | 85.4% | 80.0% | 74.4% | 79.3% |

| HBF | 82.5% | 85.3% | 85.8% | 88.6% | 90.5% | 91.7% | 93.3% | 86.8% |

| HCF | 82.4% | 91.4% | 88.6% | 90.9% | 88.9% | 86.1% | 91.7% | 88.2% |

| HCI | 71.7% | 87.4% | 89.1% | 91.2% | 89.3% | 90.2% | 92.5% | N/A |

| Health.com.au | 79.1% | 86.4% | 84.8% | 88.5% | 87.9% | 86.8% | 86.5% | 86.9% |

| Health Partners | 76.0% | 91.1% | 89.2% | 92.4% | 93.2% | 80.6% | 87.8% | 85.2% |

| HIF | 73.4% | 88.6% | 89.5% | 91.3% | 88.5% | 87.5% | 89.6% | 91.7% |

| Latrobe | 55.5% | 79.8% | 78.6% | 83.1% | 87.0% | 75.7% | 75.2% | 50.0% |

| MDHF | 30.8% | 84.3% | 78.5% | 80.1% | 80.9% | 61.5% | 70.8% | 85.7% |

| Medibank | 77.3% | 86.9% | 87.0% | 86.6% | 86.2% | 74.8% | 90.6% | 87.7% |

| NIB | 69.9% | 93.1% | 91.1% | 87.8% | 95.3% | 89.1% | 88.4% | 80.7% |

| Onemedifund | 87.2% | 91.8% | 90.2% | 94.6% | 91.1% | 80.4% | 90.9% | N/A |

| Peoplecare | 76.3% | 93.3% | 91.4% | 92.2% | 91.4% | 86.3% | 93.1% | 89.8% |

| Phoenix | 86.8% | 92.9% | 89.6% | 92.8% | 93.7% | 88.2% | 92.7% | 89.8% |

| QCH | 79.4% | 94.9% | 91.4% | 91.4% | 89.4% | 85.9% | 81.8% | 82.2% |

| St Lukes | 72.2% | 80.4% | 84.7% | 80.0% | 84.6% | 67.9% | 90.6% | 83.3% |

| Transport Health | 33.3% | 86.0% | 91.8% | 90.5% | 88.4% | 88.9% | 100.0% | N/A |

| Westfund | 71.7% | 92.4% | 88.5% | 90.1% | 90.6% | 85.8% | 79.2% | 69.4% |

| Restricted membership funds | ||||||||

| ACA | 78.5% | 92.7% | 94.1% | 94.7% | 93.0% | 83.2% | 92.4% | N/A |

| CBHS | 82.4% | 90.1% | 90.5% | 92.3% | 91.7% | 86.0% | 91.2% | 95.2% |

| Defence Health | 80.2% | 90.0% | 90.6% | 92.5% | 91.4% | 85.9% | 90.1% | 87.0% |

| Doctors' Health | 90.0% | 91.6% | 92.7% | 94.2% | 91.0% | 89.2% | 91.7% | 90.6% |

| Navy Health | 77.1% | 91.6% | 90.8% | 92.2% | 92.5% | 87.1% | 89.8% | 93.5% |

| Nurses and Midwives | 72.5% | 91.4% | 86.3% | 91.9% | 91.0% | 83.5% | 89.1% | 84.8% |

| Police Health | 76.4% | 85.6% | 84.7% | 89.0% | 90.2% | 83.2% | 87.2% | 85.9% |

| Reserve Bank | 72.8% | 90.3% | 94.0% | 95.8% | 93.9% | 91.8% | 95.0% | 92.8% |

| RT Health Fund | 73.8% | 93.0% | 90.6% | 93.6% | 90.6% | 86.3% | 93.0% | 96.5% |

| Teachers Health | 82.9% | 91.4% | 90.0% | 92.7% | 91.2% | 84.6% | 91.2% | 87.9% |

| TUH | 87.6% | 90.5% | 88.5% | 92.6% | 87.4% | 88.6% | 93.1% | 81.6% |

| Industry average | 79.6% | 90.5% | 89.0% | 90.8% | 92.0% | 87.5% | 91.3% | 88.9% |

Note: 'N/A' signifies no activity or very low activity in that state. 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

| Fund Name (Abbreviated) | % of Services with no gap or where known gap payment made | |||||||

|---|---|---|---|---|---|---|---|---|

| ACT | NSW | VIC | QLD | SA | WA | TAS | NT | |

| Open membership funds | ||||||||

| AIA Health | 90.5% | 95.2% | 97.7% | 96.8% | 99.1% | 95.3% | 91.6% | 88.9% |

| Australian Unity | 91.8% | 96.9% | 98.1% | 96.8% | 98.2% | 97.4% | 98.4% | 97.9% |

| BUPA | 94.5% | 96.8% | 99.0% | 98.3% | 99.7% | 96.8% | 99.3% | 97.7% |

| CBHS Corporate | 84.2% | 95.1% | 97.5% | 95.6% | 100.0% | 95.2% | 89.2% | N/A |

| CDH | 52.9% | 96.9% | 78.0% | 91.3% | 90.3% | 100.0% | 100.0% | N/A |

| CUA Health | 93.7% | 97.9% | 98.8% | 98.5% | 98.7% | 96.7% | 97.2% | 96.1% |

| GMHBA | 78.9% | 91.9% | 96.7% | 93.3% | 97.9% | 93.6% | 86.1% | 92.4% |

| HBF | 99.8% | 99.5% | 99.9% | 99.6% | 100.0% | 99.8% | 99.9% | 99.4% |

| HCF | 97.1% | 98.9% | 99.5% | 99.3% | 99.9% | 98.5% | 99.6% | 98.9% |

| HCI | 98.8% | 97.0% | 99.0% | 97.9% | 97.9% | 97.6% | 99.1% | N/A |

| Health.com.au | 92.7% | 95.8% | 97.5% | 97.6% | 98.7% | 98.5% | 99.7% | 97.5% |

| Health Partners | 95.4% | 97.1% | 98.6% | 97.5% | 99.8% | 97.4% | 97.4% | 100.0% |

| HIF | 92.4% | 97.5% | 98.9% | 98.2% | 99.0% | 98.0% | 99.8% | 97.2% |

| Latrobe | 98.0% | 97.8% | 99.9% | 99.3% | 99.6% | 99.6% | 99.7% | 100.0% |

| MDHF | 100.0% | 99.6% | 99.7% | 98.5% | 99.5% | 92.5% | 93.8% | 85.7% |

| Medibank | 94.0% | 96.8% | 97.4% | 95.2% | 99.4% | 89.9% | 98.5% | 96.6% |

| NIB | 70.1% | 93.4% | 92.5% | 88.2% | 95.4% | 91.0% | 88.8% | 80.7% |

| Onemedifund | 100.0% | 97.5% | 99.0% | 99.0% | 99.8% | 96.8% | 99.7% | N/A |

| Peoplecare | 94.7% | 98.3% | 99.2% | 98.2% | 99.7% | 97.9% | 99.6% | 93.5% |

| Phoenix | 95.4% | 98.5% | 98.9% | 98.4% | 99.9% | 97.6% | 100.0% | 95.9% |

| QCH | 95.6% | 98.5% | 98.9% | 98.1% | 97.7% | 97.2% | 88.6% | 90.9% |

| St Lukes | 90.3% | 89.1% | 93.8% | 93.9% | 95.2% | 77.6% | 98.6% | 83.3% |

| Transport Health | 100.0% | 95.9% | 99.0% | 97.8% | 100.0% | 99.3% | 100.0% | N/A |

| Westfund | 84.4% | 98.0% | 97.7% | 98.3% | 98.3% | 97.2% | 87.7% | 98.0% |

| Restricted membership funds | ||||||||

| ACA | 98.3% | 97.7% | 99.2% | 98.8% | 99.4% | 96.4% | 99.2% | N/A |

| CBHS | 95.8% | 97.0% | 98.3% | 97.7% | 98.7% | 97.3% | 98.7% | 98.2% |

| Defence Health | 94.9% | 97.5% | 99.0% | 98.3% | 99.6% | 98.0% | 98.9% | 95.7% |

| Doctors' Health | 97.6% | 98.2% | 98.8% | 98.9% | 99.2% | 98.7% | 98.7% | 96.2% |

| Navy Health | 94.0% | 97.6% | 98.8% | 97.9% | 99.2% | 97.5% | 98.7% | 97.8% |

| Nurses and Midwives | 92.9% | 97.5% | 98.2% | 97.7% | 98.7% | 95.9% | 98.5% | 100.0% |

| Police Health | 93.3% | 95.3% | 97.1% | 97.1% | 99.6% | 97.1% | 98.1% | 97.0% |

| Reserve Bank | 92.2% | 96.9% | 99.4% | 99.1% | 99.3% | 98.4% | 99.4% | 100.0% |

| RT Health Fund | 93.3% | 98.5% | 98.9% | 98.8% | 99.3% | 97.1% | 99.6% | 98.3% |

| Teachers Health | 95.8% | 97.8% | 98.9% | 98.6% | 99.5% | 97.7% | 99.5% | 96.0% |

| TUH | 97.1% | 97.6% | 98.0% | 98.4% | 100.0% | 97.9% | 99.3% | 86.8% |

| Industry average | 92.8% | 97.0% | 98.0% | 97.0% | 99.5% | 97.2% | 98.6% | 97.0% |

Note: 'N/A' signifies no activity or very low activity in that state. 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

General treatment (extras)

General treatment policies, also known as 'ancillary' or 'extras' provide benefits towards a range of out-of-hospital health services. The most commonly included services are dental, optical, physiotherapy and non-Pharmaceutical Benefits Scheme prescription medicines.

Table 5A shows the average proportion of service charges covered by each fund per state for all their policies and services. Table 5B shows the information according to the service being covered. Generally, higher-cost policies cover a higher proportion of charges.

General treatment

General treatment policies, provide benefits towards a range of health-related services not provided by a doctor, including, but not limited to:

- dental fees and charges

- optometry—cost of glasses and lenses

- physiotherapy, chiropractic services and other therapies including natural and complementary therapies

- prescribed medicines not covered by the Pharmaceutical Benefits Scheme.

Percentage of charges covered, all services, by state

This table indicates what proportion of total charges, associated with general treatment services, is covered by each fund's benefits. This is an average of outcomes across all of each fund's general treatment policies and services. Higher cost policies will generally cover a greater proportion of charges than indicated by this average, while cheaper policies may cover less.

Average costs covered for each service type

This additional table provides information on the proportion of the total charge for each service type covered by each fund on average, across all of the fund's general treatment policies.

This is intended to provide a broad comparative indicator of fund general treatment benefits to allow comparisons between funds and should not be regarded as an indicator of how much of a bill for any particular service will be covered.

Ambulance

Some funds do not provide ambulance cover through any of their general treatment policies but offer this as a component of hospital cover. These funds show as 'N/A' under the ambulance column. Most ambulance services in Queensland and Tasmania are provided free to residents of those states.

Preferred providers

Many funds establish 'preferred provider' or 'participating provider' arrangements with some suppliers of general treatment services. Those providers offer an agreed charge for fund members, resulting in lower out of pocket costs for members after fund benefits are taken into account. It is usually worth checking with your fund to see if a suitable preferred provider is available in your area.

Fund dental and eyecare centres

In some states, some funds operate their own dental and optical centres. These are usually only located in capital cities or major population centres.

Consumers who choose to use a fund's own dental or optical centre will normally get services at a lower out of pocket cost.

| Fund Name (Abbreviated) | % General treatment (extras) Charges covered | |||||||

|---|---|---|---|---|---|---|---|---|

| ACT | NSW | VIC | QLD | SA | WA | TAS | NT | |

| Open membership funds | ||||||||

| AIA Health | 54.5% | 53.1% | 54.4% | 53.7% | 56.0% | 57.5% | 56.3% | 65.1% |

| Australian Unity | 44.7% | 46.9% | 49.8% | 50.2% | 52.8% | 49.2% | 47.0% | 52.1% |

| BUPA | 46.6% | 50.8% | 49.7% | 53.4% | 56.9% | 59.3% | 51.6% | 60.0% |

| CBHS Corporate | 49.8% | 51.6% | 52.9% | 50.6% | 55.9% | 52.2% | 54.2% | N/A |

| CDH | 37.0% | 37.1% | 39.9% | 36.3% | 45.2% | 39.3% | 34.8% | N/A |

| CUA Health | 43.9% | 53.0% | 48.8% | 48.6% | 53.1% | 48.6% | 51.5% | 40.6% |

| GMHBA | 50.4% | 52.2% | 49.5% | 53.2% | 52.4% | 50.7% | 48.0% | 52.0% |

| HBF | 44.5% | 49.0% | 48.7% | 48.9% | 52.0% | 56.7% | 48.0% | 51.7% |

| HCF | 50.9% | 50.5% | 56.6% | 57.5% | 62.4% | 61.0% | 53.2% | 54.3% |

| HCI | 50.7% | 53.7% | 53.1% | 49.5% | 53.0% | 48.2% | 46.5% | 49.0% |

| Health.com.au | 50.5% | 51.2% | 52.5% | 51.2% | 54.1% | 53.6% | 53.9% | 48.7% |

| Health Partners | 53.2% | 54.1% | 44.6% | 42.4% | 58.1% | 46.6% | 45.3% | 43.9% |

| HIF | 42.5% | 46.1% | 46.4% | 47.0% | 49.6% | 47.5% | 46.5% | 46.6% |

| Latrobe | 28.1% | 32.7% | 36.0% | 34.6% | 39.2% | 43.0% | 34.6% | 29.4% |

| MDHF | 47.6% | 54.0% | 55.1% | 54.9% | 51.5% | 43.7% | 50.5% | 45.8% |

| Medibank | 48.5% | 51.7% | 54.0% | 55.6% | 59.6% | 58.8% | 53.9% | 60.7% |

| NIB | 55.6% | 56.0% | 60.6% | 56.4% | 60.9% | 63.2% | 56.0% | 59.6% |

| Onemedifund | 52.4% | 53.4% | 56.2% | 53.6% | 56.0% | 57.3% | 56.8% | N/A |

| Peoplecare | 46.5% | 49.7% | 48.9% | 47.6% | 51.9% | 45.9% | 46.2% | 48.5% |

| Phoenix | 46.7% | 52.6% | 52.1% | 53.9% | 56.2% | 52.5% | 51.6% | 52.6% |

| QCH | 48.2% | 49.2% | 49.6% | 51.7% | 49.6% | 48.6% | 50.6% | 46.3% |

| St Lukes | 55.2% | 63.0% | 59.1% | 60.2% | 65.3% | 62.5% | 60.3% | 59.1% |

| Transport Health | 48.3% | 47.8% | 53.0% | 46.5% | 50.7% | 47.6% | 52.3% | 41.3% |

| Westfund | 40.7% | 49.4% | 45.2% | 51.4% | 49.5% | 43.4% | 40.1% | 46.4% |

| Restricted membership funds | ||||||||

| ACA | 57.8% | 58.4% | 59.1% | 59.9% | 61.6% | 59.3% | 54.6% | 50.1% |

| CBHS | 42.6% | 47.8% | 48.8% | 50.2% | 52.7% | 49.9% | 47.8% | 46.1% |

| Defence Health | 42.8% | 45.9% | 48.2% | 47.9% | 43.3% | 46.7% | 46.2% | 50.4% |

| Doctors' Health | 54.4% | 53.5% | 55.3% | 55.8% | 58.2% | 59.0% | 55.7% | 57.2% |

| Navy Health | 45.2% | 48.4% | 51.8% | 50.3% | 56.2% | 52.0% | 47.3% | 50.0% |

| Nurses and Midwives | 42.8% | 52.1% | 49.8% | 51.0% | 53.7% | 54.3% | 46.2% | 46.0% |

| Police Health | 66.7% | 66.7% | 67.4% | 67.8% | 70.9% | 69.0% | 67.4% | 68.0% |

| Reserve Bank | 70.6% | 73.0% | 75.7% | 75.9% | 81.4% | 76.7% | 75.2% | 90.0% |

| RT Health Fund | 37.7% | 47.7% | 43.9% | 46.2% | 49.4% | 43.6% | 41.9% | 42.1% |

| Teachers Health | 42.2% | 47.7% | 47.8% | 47.5% | 51.5% | 50.0% | 47.1% | 47.2% |

| TUH | 45.7% | 49.1% | 48.4% | 54.9% | 52.6% | 50.1% | 53.1% | 48.4% |

| Industry average | 48.0% | 50.7% | 52.3% | 54.1% | 57.6% | 57.1% | 54.3% | 59.5% |

Note: 'N/A' signifies no activity in that state. 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

| Average amount of costs covered by service | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Fund Name (Abbreviated) | Dental [1] | Optical [1] | Physiotherapy | Chiropractic | Pharmacy | Podiatry | Natural therapies | Ambulance | Acupuncture | Psychology/Group therapy | Preventative health | Hearing aids | Occupational therapy |

| Open membership funds | |||||||||||||

| AIA Health | 51.8% | 54.5% | 58.1% | 58.0% | 27.3% | 62.8% | 54.4% | 100.0% | 52.4% | 55.7% | 76.4% | 12.5% | 58.3% |

| Australian Unity | 45.2% | 65.5% | 60.8% | 46.9% | 38.0% | 45.2% | 46.8% | 98.6% | 38.9% | 33.2% | 74.3% | 16.0% | 42.5% |

| BUPA | 56.0% | 56.5% | 47.0% | 48.3% | 34.7% | 48.8% | 38.3% | 100.0% | 38.3% | 41.2% | 36.5% | 18.8% | 33.9% |

| CBHS Corporate | 49.7% | 56.3% | 52.6% | 60.6% | 41.9% | 53.8% | 52.6% | 96.5% | 56.9% | 44.0% | N/A | 31.4% | 30.2% |

| CDH | 37.3% | 52.7% | 42.2% | 39.4% | 42.0% | 33.1% | 25.9% | 100.0% | 42.9% | 17.3% | 31.4% | N/A | 29.1% |

| CUA Health | 51.3% | 58.8% | 38.8% | 42.9% | 28.6% | 50.2% | 38.3% | 99.5% | 43.0% | 34.4% | 39.4% | 56.4% | 38.8% |

| GMHBA | 50.4% | 57.2% | 47.7% | 49.5% | 33.8% | 48.3% | 30.4% | 86.8% | 46.5% | 43.8% | 66.6% | 27.3% | 42.2% |

| HBF | 56.1% | 58.1% | 47.8% | 52.7% | 50.4% | 49.0% | 50.3% | 100.0% | N/A | 40.0% | 94.9% | 38.2% | 44.0% |

| HCF | 58.5% | 57.3% | 44.2% | 42.3% | 35.4% | 39.9% | 33.7% | 100.0% | 31.1% | 45.7% | 42.6% | 30.8% | 48.3% |

| HCI | 51.3% | 53.0% | 41.3% | 50.2% | 44.6% | 43.6% | 51.2% | 100.0% | 54.8% | 29.7% | 67.4% | 47.0% | 38.9% |

| Health.com.au | 49.0% | 49.2% | 57.8% | 58.2% | 28.8% | 54.2% | 57.4% | 100.0% | 57.0% | 51.6% | na | 21.1% | 54.7% |

| Health Partners | 61.6% | 54.4% | 59.4% | 43.5% | 46.4% | 34.4% | 27.7% | 100.0% | 29.3% | 35.8% | 66.3% | 32.3% | 46.1% |

| HIF | 48.2% | 58.4% | 39.0% | 39.6% | 40.5% | 35.0% | 22.8% | 99.3% | 20.9% | 32.1% | 33.8% | 29.5% | 33.7% |

| Latrobe | 33.5% | 55.2% | 32.4% | 36.2% | 11.7% | 36.2% | 23.4% | 76.4% | 43.5% | 28.9% | 38.1% | 13.4% | 35.2% |

| MDHF | 61.3% | 63.0% | 40.6% | 43.9% | 28.6% | 44.2% | 36.7% | 81.0% | 33.1% | 26.8% | 47.8% | 34.0% | 32.0% |

| Medibank | 53.5% | 68.9% | 46.5% | 51.7% | 29.5% | 50.7% | 52.2% | 100.0% | 41.1% | 32.2% | 64.1% | 26.9% | 35.4% |

| NIB | 57.8% | 54.1% | 60.7% | 60.7% | 43.7% | 58.1% | 61.1% | 100.0% | 59.2% | 60.6% | 47.2% | 19.3% | 66.1% |

| Onemedifund | 59.3% | 52.2% | 52.0% | 47.2% | 40.5% | 44.1% | 40.6% | 96.5% | 35.7% | 37.1% | 86.4% | 34.3% | 33.5% |

| Peoplecare | 48.6% | 60.3% | 39.2% | 41.7% | 35.3% | 38.4% | 37.7% | 99.6% | 39.5% | 37.6% | 67.3% | 35.9% | 39.0% |

| Phoenix | 56.7% | 66.1% | 43.6% | 44.9% | 38.0% | 48.2% | 46.6% | 96.4% | 40.5% | 40.1% | 48.1% | 42.1% | 43.2% |

| QCH | 51.7% | 60.1% | 43.7% | 55.6% | 36.8% | 60.7% | 33.3% | na | 41.2% | 42.6% | 46.1% | 35.0% | 38.0% |

| St Lukes | 64.5% | 75.7% | 50.1% | 49.7% | 41.4% | 46.1% | 41.5% | 74.8% | 44.1% | 45.5% | 59.7% | 45.4% | 49.1% |

| Transport Health | 55.0% | 57.5% | 43.6% | 52.3% | 30.9% | 50.2% | 41.1% | 100.0% | 34.6% | 27.6% | 59.5% | 27.4% | 29.2% |

| Westfund | 51.5% | 56.2% | 45.2% | 51.3% | 38.8% | 46.1% | 38.0% | 100.0% | 34.8% | 39.6% | 82.7% | 41.0% | 43.6% |

| Restricted membership funds | |||||||||||||

| ACA | 61.7% | 70.6% | 40.5% | 46.7% | 44.4% | 72.5% | 37.6% | 100.0% | 34.0% | 46.6% | N/A | 42.9% | 65.9% |

| CBHS | 49.3% | 53.3% | 49.8% | 59.0% | 40.8% | 42.3% | 44.1% | 95.0% | 44.2% | 38.1% | N/A | 38.5% | 33.4% |

| Defence Health | 46.0% | 52.5% | 48.7% | 40.6% | 31.5% | 48.4% | 35.9% | 100.0% | 31.2% | 43.3% | 74.7% | 32.0% | 44.5% |

| Doctors' Health | 59.3% | 63.5% | 43.3% | 0.0% | 40.7% | 50.3% | 40.3% | N/A | N/A | 46.8% | 33.0% | 21.4% | 33.7% |

| Navy Health | 46.9% | 58.6% | 51.5% | 58.1% | 44.0% | 52.0% | 43.7% | 98.5% | N/A | 40.2% | 100.0% | 30.0% | 32.9% |

| Nurses and Midwives | 52.3% | 60.4% | 44.1% | 58.9% | 41.8% | 54.2% | 44.5% | 100.0% | 40.8% | 39.9% | 42.4% | 28.0% | 54.3% |

| Police Health | 69.7% | 66.8% | 75.2% | 76.6% | 45.3% | 68.1% | 39.2% | 99.9% | 73.2% | 76.3% | 100.0% | 41.0% | 67.8% |

| Reserve Bank | 74.4% | 71.0% | 68.2% | 71.1% | 60.9% | 78.4% | 76.9% | 97.8% | 72.4% | 74.6% | 57.6% | 78.3% | 66.6% |

| RT Health Fund | 44.3% | 60.2% | 46.7% | 47.1% | 38.1% | 44.7% | 42.5% | 100.0% | 47.3% | 17.3% | 36.6% | 30.8% | 31.0% |

| Teachers Health | 50.8% | 49.2% | 42.8% | 55.3% | 38.4% | 47.4% | 44.1% | 99.8% | 38.5% | 37.1% | 37.1% | 38.9% | 56.7% |

| TUH | 58.4% | 56.0% | 49.4% | 52.8% | 35.4% | 56.8% | 50.5% | 100.0% | 42.6% | 40.2% | 49.1% | 45.1% | 35.8% |

| Industry average | 54.4% | 59.8% | 48.2% | 49.9% | 36.2% | 49.0% | 45.0% | 99.5% | 40.4% | 40.5% | 55.6% | 28.4% | 42.4% |

[1] For some funds, the data does not take account of discounts at some providers or fund dental/optical centres.

Note: All percentages based on health fund reporting to APRA. 'N/A' signifies no activity and 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

Finances and costs

All health funds are required to meet financial management standards, to ensure their members' contributions are protected. Generally, funds aim to set premium levels so their income from contributions covers the expected cost of benefits plus the fund's administration costs.

The percentage of contribution income which goes towards administration and management expenses is a key measure of fund efficiency.

The regulation of health fund finances

The Private Health Insurance Act 2007 (the Act) specifies solvency and capital adequacy standards for funds to meet and outlines financial management and reporting requirements for all funds.

The Private Health Insurance (Prudential Supervision) Act 2015 (the Prudential Supervision Act) ensures that private health insurers must comply with prudential standards made by APRA and with directions given by APRA. APRA has monitoring and investigative powers in relation to private health insurers in order to monitor the financial performance of the funds and ensure that they meet prudential requirements.

APRA produces an annual publication providing financial and operational statistics for the funds for each financial year.[3] Information included in the Financial Performance table (Table 6) is drawn from data collected by APRA.

Premium increases

Under the Act, health funds require the approval of the Minister for Health before they can raise their premiums.

The Minister assesses premium applications to ensure proposed increases are kept to the minimum necessary. This takes into consideration fund solvency requirements, forecast benefit payments and prudential requirements, while also ensuring the affordability and value of private health insurance as a product.

Benefits as a percentage of contributions

This column shows the percentage of total contributions, received by the fund, returned to contributors in benefits. Funds will generally aim to set premium levels so that contribution income covers the expected costs of benefits plus the fund's administration costs.

A very high percentage of contributions returned as benefits may not necessarily be a positive factor for consumers, particularly if it means that the fund is making a loss on its health insurance business. This indicator should therefore be considered in conjunction with other factors, such as Surplus (- loss) and Management Expenses.

Management expenses

Management expenses are the costs of administering the fund. They include items such as rent, staff salaries and marketing costs.

As a percentage of contribution income

This figure is regarded as a key measure of fund efficiency. In this table, management expenses are shown as a proportion of total fund contributions.

Per average policy

A comparison of the relative amount each fund spends on administration costs is also demonstrated through provision of information on the level of management expenses per membership by each fund.

On average, restricted membership funds have lower management expenses as a proportion of benefits paid then open membership funds. This is partially due to lower expenditure on marketing. However, unusually low management expenses by some restricted membership funds can also be the result of those funds receiving free or subsidised administrative services from the organisations with which they are associated.

Surplus (-loss) from health insurance

The surplus or loss (indicated as a negative figure) made by the fund in 2019–20 from their health insurance business is expressed as a percentage of the fund's contribution income. This does not take account of additional income that the fund may derive from investment or other non-health insurance activities.

All health funds maintain a sufficient level of reserves to cover losses from year to year. However, funds with high or continuing losses might be expected to have to increase premiums by a higher amount than other funds.

Overall profit (-loss) as a percentage of total revenue

The overall profit or loss (indicated as a negative figure) takes account of additional income made by the fund, mainly through investment. This is shown as a percentage of all revenue received by the fund to allow a comparison of performance between funds of differing sizes. Overall profit takes into account tax that is paid for a small amount of funds.

Not-for-profit fund

If a health fund is listed as 'not-for-profit' this means it is a mutual organisation, with the premiums paid into the fund used to operate the business and cover benefits for members.

'For-profit' funds aim to return a profit to their owners (which may be another health fund or corporation) or shareholders.

| Fund name (Abbreviated) | Benefits as % contributions | Management expenses | Surplus (-Loss) from health insurance | Overall Profit (- Loss) as % total revenue | Not for profit fund | |

| as % of contribution income | Per average policy | |||||

| Open membership funds | ||||||

| AIA Health | 105.6% | 30.0% | $1,076 | -35.6% | -28.7% | No |

| Australian Unity | 83.0% | 11.0% | $417 | 6.0% | 4.4% | No |

| BUPA | 88.3% | 7.8% | $296 | 3.9% | 3.4% | No |

| CBHS Corporate | 110.2% | 37.1% | 1,273 | -47.3% | -62.2% | No |

| CDH | 84.9% | 14.8% | $654 | 0.2% | 0.6% | Yes |

| CUA Health | 84.7% | 9.9% | $369 | 5.4% | 4.1% | No |

| GMHBA | 85.0% | 12.2% | $445 | 2.8% | 1.8% | Yes |

| HBF | 88.6% | 11.6% | $383 | -0.2% | 2.2% | Yes |

| HCF | 93.2% | 11.0% | $422 | -4.2% | -2.8% | Yes |

| HCI | 83.4% | 11.1% | $477 | 5.5% | 5.1% | Yes |

| Health.com.au | 90.8% | 7.1% | $223 | 2.1% | 2.4% | No |

| Health Partners | 91.9% | 9.8% | $369 | -1.7% | 0.0% | Yes |

| HIF | 86.9% | 11.9% | $390 | 1.2% | 2.1% | Yes |

| Latrobe | 94.8% | 11.7% | $467 | -6.5% | -8.4% | Yes |

| MDHF | 89.0% | 9.1% | $321 | 1.9% | 0.5% | Yes |

| Medibank | 85.7% | 8.0% | $284 | 6.3% | 4.9% | No |

| NIB | 84.0% | 10.5% | $355 | 5.5% | 8.3% | No |

| Onemedifund | 84.4% | 9.2% | $524 | 6.5% | 5.3% | No |

| Peoplecare | 87.7% | 10.0% | $433 | 2.3% | 1.6% | Yes |

| Phoenix | 90.4% | 10.1% | $482 | -0.5% | 0.1% | Yes |

| QCH | 88.9% | 11.4% | $537 | -0.3% | 1.1% | No |

| St Lukes | 91.3% | 11.0% | $478 | -2.3% | -1.9% | Yes |

| Transport Health | 84.6% | 12.7% | $472 | 2.7% | 2.8% | No |

| Westfund | 87.1% | 13.9% | $562 | -1.0% | -1.7% | Yes |

| Restricted membership funds | ||||||

| ACA | 88.4% | 12.2% | $654 | -0.7% | -1.0% | Yes |

| CBHS | 96.2% | 8.9% | $391 | -5.1% | -3.6% | Yes |

| Defence Health | 92.0% | 6.5% | $272 | 1.4% | 2.8% | Yes |

| Doctors' Health | 88.0% | 10.2% | $535 | 1.7% | 2.4% | No |

| Navy Health | 90.3% | 9.7% | $402 | 0.0% | 0.3% | Yes |

| Nurses and Midwives | 99.8% | 11.8% | $476 | -11.6% | -11.7% | Yes |

| Police Health (1) | 92.2% | 9.4% | $478 | -1.6% | -1.0% | Yes |

| Reserve Bank | 86.7% | 12.8% | $888 | 0.5% | 1.9% | Yes |

| RT Health Fund | 85.5% | 16.1% | $746 | -1.5% | -3.3% | Yes |

| Teachers Health | 89.6% | 8.1% | $365 | 2.3% | 2.8% | Yes |

| TUH | 86.7% | 9.2% | $455 | 4.1% | 2.5% | Yes |

| Industry result | 88.0% | 9.2% | $343 | 2.7% | 2.9% | |

(1) these figures are reflective of the Police Health (amalgamated) Group

Health fund operations by state or territory

Some funds have little presence in most states but may have a large market share in one state or territory. Every fund will still have agreements with hospitals throughout Australia even if they don't have a local branch network or a significant proportion of policyholders in each state. Australian health insurance policies are usually priced according to the policyholder's state of residence, but the benefits extend nation-wide.

Health fund operations by state or territory

These separate tables for each state/territory are therefore provided to give an indication of the extent and importance of each fund's business in each area.

Most fund websites allow members to view fund information, join or change their policy and submit claims. Links to all health fund websites are available at Table 1—Health fund listing and contact details.

Percentage market share

This column indicates how much of the total health insurance business within each state or territory each fund accounts for. It is an indicator of the size and significance of each fund within each state.

Funds with a significant market share in the relevant state or territory can normally be expected to have more extensive networks of branch offices, agencies, agreement hospitals and preferred ancillary providers in those states/territories. They are also more likely to obtain the participation of doctors in their gap cover arrangements. However, funds participating in schemes such as the Australian Health Services Alliance (AHSA) will generally have access to a wide range of agreement hospitals in all states.[4]

Percentage of fund's membership in state

This column indicates how much of each fund's health insurance membership is within each state. It is an indicator of how significant that state is to each fund's health insurance business.

In general, funds can be expected to design their policies (benefits, conditions, contracts, etc.) to suit the arrangements applying in the states in which they have a significant proportion of business. However, some nationally-based funds tailor their policies and prices to take account of different state arrangements.

Health fund costs differ from state to state, which accounts for the variation in premiums across states.

Agreement hospitals[5]

All health funds establish agreements with private hospitals and day hospitals for the treatment of their members. These agreements generally provide for the fund to meet all of the private hospital's charges for treatment of the fund's members. The member is not required to pay any amount to the hospital, other than any agreed excess or co-payment and any incidental charges that may apply for certain extra services (e.g. television rental or internet).[6]

Where a fund has a comparatively low number of agreements with private hospitals or private day hospitals, this is an indicator that consumer choices about the location of their treatment may be limited. Treatment at a non-agreement hospital will mean a significantly higher out of pocket cost for the patient.

While funds do not have agreements with public hospitals, all funds will fully cover hospital costs for treatment as a private patient in a public hospital unless the particular treatment is excluded under the individual's policy, there is an extra charge for a private room or similar extra costs.

Fund outlets—retail offices and agencies

Retail offices are full-service offices operated by health funds with staff employed by the fund.

Agencies are generally limited service outlets operated by the fund or under arrangements with pharmacies, credit unions, etc.

The table indicates whether the fund operates retail offices and/or agencies in the state or territory.

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||

| Open membership funds | ||||||

| AIA Health | 0.2% | 35.4% | 89 | 91 | ||

| Australian Unity | 1.4% | 17.8% | 92 | 91 | ||

| BUPA | 24.4% | 31.6% | 88 | 74 | Yes | |

| CBHS Corporate | 0.0% | 57.9% | 94 | 89 | ||

| CDH | 0.1% | 77.0% | 79 | 52 | Yes | |

| CUA Health | 0.4% | 24.8% | 92 | 87 | Yes | |

| GMHBA | 1.1% | 16.8% | 96 | 87 | ||

| HBF | 0.7% | 3.3% | 86 | 93 | ||

| HCF | 20.1% | 56.8% | 85 | 88 | Yes | |

| HCI | 0.0% | 11.6% | 94 | 109 | ||

| Health.com.au | 0.5% | 34.3% | 79 | 71 | ||

| Health Partners | 0.1% | 3.2% | 96 | 87 | ||

| HIF | 0.3% | 11.6% | 95 | 91 | ||

| Latrobe | 0.2% | 8.0% | 79 | 56 | ||

| MDHF | 0.1% | 11.2% | 79 | 56 | Yes | |

| Medibank | 23.1% | 28.2% | 91 | 76 | Yes | |

| NIB | 14.5% | 51.8% | 92 | 93 | Yes | |

| Onemedifund | 0.1% | 41.6% | 96 | 87 | ||

| Peoplecare | 0.7% | 47.2% | 96 | 87 | Yes | |

| Phoenix | 0.2% | 43.8% | 95 | 89 | Yes | |

| QCH | 0.0% | 1.6% | 94 | 88 | ||

| St Lukes | 0.1% | 3.3% | 78 | 55 | ||

| Transport Health | 0.0% | 12.8% | 96 | 87 | ||

| Westfund | 1.5% | 57.0% | 96 | 92 | Yes | |

| Restricted membership funds | ||||||

| ACA | 0.1% | 57.2% | 92 | 89 | Yes | |

| CBHS | 2.2% | 46.4% | 94 | 89 | ||

| Defence Health | 1.2% | 18.3% | 92 | 92 | Yes | |

| Doctors' Health | 0.4% | 40.3% | 93 | 92 | ||

| Navy Health | 0.3% | 29.1% | 95 | 91 | ||

| Nurses and Midwives | 0.1% | 48.9% | 92 | 91 | ||

| Police | 0.1% | 4.6% | 95 | 91 | ||

| Reserve Bank | 0.1% | 61.0% | 96 | 87 | Yes | |

| RT Health Fund | 0.7% | 49.7% | 96 | 87 | Yes | |

| Teachers Health | 5.1% | 67.7% | 92 | 91 | Yes | |

| TUH | 0.1% | 5.4% | 95 | 89 | ||

[1] Agreement hospitals data is sourced from privatehealth.gov.au as of 9 October 2020

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||

| Open membership funds | ||||||

| AIA Health | 0.4% | 39.0% | 76 | 69 | ||

| Australian Unity | 6.6% | 60.9% | 76 | 72 | ||

| BUPA | 23.0% | 21.4% | 75 | 62 | Yes | |

| CBHS Corporate | 0.0% | 15.3% | 72 | 72 | ||

| CDH | 0.0% | 11.7% | 74 | 63 | ||

| CUA Health | 0.5% | 18.4% | 73 | 70 | Yes | Yes |

| GMHBA | 5.7% | 64.2% | 76 | 69 | Yes | Yes |

| HBF | 1.1% | 3.5% | 65 | 75 | Yes | Yes |

| HCF | 7.6% | 15.4% | 67 | 50 | Yes | |

| HCI | 0.1% | 22.8% | 77 | 83 | ||

| Health.com.au | 0.7% | 35.3% | 67 | 57 | ||

| Health Partners | 0.2% | 7.9% | 76 | 69 | ||

| HIF | 0.5% | 15.4% | 76 | 72 | ||

| Latrobe | 2.4% | 87.3% | 74 | 63 | Yes | Yes |

| MDHF | 0.9% | 83.3% | 74 | 63 | Yes | Yes |

| Medibank | 33.0% | 29.0% | 70 | 52 | Yes | |

| NIB | 8.6% | 22.0% | 72 | 76 | Yes | |

| Onemedifund | 0.1% | 24.7% | 76 | 69 | ||

| Peoplecare | 0.7% | 31.9% | 76 | 69 | Yes | |

| Phoenix | 0.2% | 26.2% | 74 | 72 | ||

| QCH | 0.0% | 1.0% | 75 | 70 | ||

| St Lukes | 0.1% | 4.8% | 74 | 63 | ||

| Transport Health | 0.3% | 71.1% | 76 | 69 | ||

| Westfund | 0.1% | 4.1% | 76 | 73 | ||

| Restricted membership funds | ||||||

| ACA | 0.0% | 13.0% | 75 | 71 | ||

| CBHS | 1.6% | 24.2% | 72 | 72 | ||

| Defence Health | 2.7% | 29.7% | 77 | 77 | Yes | Yes |

| Doctors' Health | 0.4% | 29.3% | 76 | 73 | ||

| Navy Health | 0.4% | 27.3% | 76 | 73 | Yes | |

| Nurses and Midwives | 0.1% | 25.0% | 74 | 73 | ||

| Police | 0.1% | 7.5% | 76 | 72 | ||

| Reserve Bank | 0.0% | 23.2% | 76 | 69 | ||

| RT Health Fund | 0.2% | 11.9% | 76 | 69 | ||

| Teachers Health | 1.6% | 15.3% | 74 | 73 | ||

| TUH | 0.1% | 4.1% | 74 | 72 | ||

[1] Agreement hospitals data is sourced from privatehealth.gov.au as of 9 October 2020

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||

| Open membership funds | ||||||

| AIA Health | 0.2% | 16.2% | 52 | 45 | ||

| Australian Unity | 1.9% | 12.7% | 50 | 50 | ||

| BUPA | 30.9% | 21.3% | 50 | 45 | Yes | |

| CBHS Corporate | 0.0% | 11.7% | 50 | 50 | ||

| CDH | 0.0% | 9.0% | 48 | 36 | ||

| CUA Health | 1.7% | 50.6% | 50 | 47 | Yes | Yes |

| GMHBA | 1.3% | 10.8% | 51 | 49 | ||

| HBF | 0.7% | 1.7% | 45 | 51 | ||

| HCF | 8.2% | 12.4% | 49 | 38 | Yes | |

| HCI | 0.0% | 10.0% | 57 | 61 | ||

| Health.com.au | 0.5% | 18.5% | 42 | 38 | ||

| Health Partners | 0.1% | 3.1% | 51 | 49 | ||

| HIF | 0.4% | 8.7% | 50 | 51 | ||

| Latrobe | 0.1% | 2.8% | 48 | 36 | ||

| MDHF | 0.0% | 2.5% | 48 | 36 | ||

| Medibank | 31.8% | 20.8% | 50 | 44 | Yes | |

| NIB | 6.9% | 13.1% | 52 | 48 | Yes | |

| Onemedifund | 0.1% | 12.9% | 51 | 49 | ||

| Peoplecare | 0.3% | 11.2% | 51 | 49 | ||

| Phoenix | 0.1% | 14.4% | 50 | 50 | ||

| QCH | 2.3% | 94.9% | 50 | 48 | Yes | Yes |

| St Lukes | 0.1% | 3.2% | 48 | 36 | ||

| Transport Health | 0.1% | 11.2% | 51 | 49 | ||

| Westfund | 1.7% | 34.1% | 50 | 49 | Yes | |

| Restricted membership funds | ||||||

| ACA | 0.1% | 20.0% | 50 | 48 | ||

| CBHS | 1.3% | 15.0% | 50 | 50 | ||

| Defence Health | 3.5% | 29.0% | 49 | 48 | Yes | |

| Doctors' Health | 0.4% | 20.5% | 50 | 49 | ||

| Navy Health | 0.4% | 19.7% | 50 | 51 | ||

| Nurses and Midwives | 0.0% | 10.1% | 51 | 49 | ||

| Police | 0.7% | 32.9% | 50 | 51 | ||

| Reserve Bank | 0.0% | 6.6% | 51 | 49 | ||

| RT Health Fund | 0.8% | 33.7% | 51 | 49 | Yes | |

| Teachers Health | 0.5% | 3.7% | 51 | 49 | ||

| TUH | 2.9% | 89.0% | 50 | 50 | Yes | |

[1] Agreement hospitals data is sourced from privatehealth.gov.au as of 9 October 2020

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||||||||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||||||||

| Open membership funds | ||||||||||||

| AIA Health | 0.1% | 2.2% | 25 | 24 | ||||||||

| Australian Unity | 1.4% | 4.3% | 26 | 25 | ||||||||

| BUPA | 46.0% | 14.1% | 26 | 27 | Yes | |||||||

| CBHS Corporate | 0.0% | 3.4% | 25 | 27 | ||||||||

| CDH | 0.0% | 1.0% | 23 | 17 | ||||||||

| CUA Health | 0.1% | 1.7% | 25 | 23 | ||||||||

| GMHBA | 0.4% | 1.5% | 23 | 28 | ||||||||

| HBF | 0.5% | 0.5% | 25 | 23 | ||||||||

| HCF | 8.5% | 5.7% | 22 | 20 | Yes | |||||||

| HCI | 0.0% | 2.3% | 28 | 33 | ||||||||

| Health.com.au | 0.2% | 3.2% | 27 | 22 | ||||||||

| Health Partners | 7.5% | 84.3% | 23 | 28 | Yes | Yes | ||||||

| HIF | 0.3% | 2.7% | 26 | 27 | ||||||||

| Latrobe | 0.1% | 0.6% | 23 | 17 | ||||||||

| MDHF | 0.1% | 2.3% | 23 | 17 | ||||||||

| Medibank | 22.3% | 6.4% | 25 | 22 | Yes | |||||||

| NIB | 4.0% | 3.4% | 23 | 27 | ||||||||

| Onemedifund | 0.1% | 4.8% | 23 | 28 | ||||||||

| Peoplecare | 0.3% | 4.7% | 23 | 28 | ||||||||

| Phoenix | 0.2% | 11.1% | 25 | 27 | ||||||||

| QCH | 0.0% | 0.3% | 25 | 27 | ||||||||

| St Lukes | 0.1% | 1.5% | 23 | 17 | ||||||||

| Transport Health | 0.0% | 1.9% | 23 | 28 | ||||||||

| Westfund | 0.2% | 1.7% | 25 | 29 | ||||||||

| Restricted membership funds | ||||||||||||

| ACA | 0.0% | 3.5% | 26 | 26 | ||||||||

| CBHS | 0.9% | 4.6% | 25 | 27 | ||||||||

| Defence Health | 2.4% | 8.6% | 27 | 30 | Yes | |||||||

| Doctors' Health | 0.2% | 3.5% | 26 | 28 | ||||||||

| Navy Health | 0.3% | 5.6% | 26 | 28 | ||||||||

| Nurses and Midwives | 0.1% | 6.9% | 23 | 27 | ||||||||

| Police | 1.6% | 31.7% | 26 | 27 | Yes | |||||||

| Reserve Bank | 0.0% | 3.3% | 23 | 28 | ||||||||

| RT Health Fund | 0.1% | 1.7% | 23 | 28 | ||||||||

| Teachers Health | 2.1% | 6.5% | 23 | 27 | ||||||||

| TUH | 0.0% | 0.4% | 25 | 27 | ||||||||

[1] Agreement hospitals data is sourced from privatehealth.gov.au as of 9 October 2020

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||||||||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||||||||

| Open membership funds | ||||||||||||

| AIA Health | 0.1% | 4.6% | 19 | 21 | ||||||||

| Australian Unity | 0.5% | 2.4% | 21 | 22 | ||||||||

| BUPA | 12.1% | 6.3% | 20 | 18 | Yes | |||||||

| CBHS Corporate | 0.0% | 8.3% | 21 | 22 | ||||||||

| CDH | 0.0% | 0.4% | 18 | 14 | ||||||||

| CUA Health | 0.1% | 2.7% | 21 | 21 | Yes | |||||||

| GMHBA | 0.7% | 4.5% | 22 | 21 | ||||||||

| HBF | 49.9% | 90.4% | 25 | 23 | Yes | Yes | ||||||

| HCF | 5.0% | 5.6% | 18 | 14 | Yes | |||||||

| HCI | 0.0% | 1.3% | 23 | 25 | ||||||||

| Health.com.au | 0.2% | 4.9% | 18 | 16 | ||||||||

| Health Partners | 0.0% | 0.5% | 22 | 21 | ||||||||

| HIF | 3.4% | 60.1% | 21 | 23 | Yes | Yes | ||||||

| Latrobe | 0.0% | 0.3% | 18 | 14 | ||||||||

| MDHF | 0.0% | 0.3% | 18 | 14 | ||||||||

| Medibank | 21.0% | 10.3% | 21 | 20 | Yes | |||||||

| NIB | 3.7% | 5.3% | 21 | 25 | ||||||||

| Onemedifund | 0.1% | 11.0% | 22 | 21 | ||||||||

| Peoplecare | 0.1% | 2.6% | 22 | 21 | ||||||||

| Phoenix | 0.0% | 2.6% | 21 | 22 | ||||||||

| QCH | 0.0% | 0.5% | 21 | 22 | ||||||||

| St Lukes | 0.0% | 0.5% | 18 | 14 | ||||||||

| Transport Health | 0.0% | 1.7% | 22 | 21 | ||||||||

| Westfund | 0.1% | 1.6% | 21 | 23 | ||||||||

| Restricted membership funds | ||||||||||||

| ACA | 0.0% | 4.0% | 21 | 21 | ||||||||

| CBHS | 0.8% | 6.9% | 21 | 22 | ||||||||

| Defence Health | 0.7% | 4.4% | 20 | 23 | Yes | |||||||

| Doctors' Health | 0.1% | 2.6% | 21 | 23 | ||||||||

| Navy Health | 0.2% | 7.1% | 21 | 23 | ||||||||

| Nurses and Midwives | 0.0% | 5.0% | 21 | 23 | ||||||||

| Police | 0.4% | 12.7% | 21 | 23 | ||||||||

| Reserve Bank | 0.0% | 3.0% | 22 | 21 | ||||||||

| RT Health Fund | 0.1% | 1.6% | 22 | 21 | ||||||||

| Teachers Health | 0.6% | 3.2% | 21 | 23 | ||||||||

| TUH | 0.0% | 0.3% | 21 | 22 | ||||||||

[1] Agreement hospitals data is sourced from privatehealth.gov.au as of 9 October 2020

| Fund name (Abbreviated) | % Fund market share this state | % Fund's membership in this state | Agreement hospitals [1] | Fund outlets | ||||||||

| Private hospitals | Private day hospitals | Retail offices | Agencies | |||||||||

| Open membership funds | ||||||||||||

| AIA Health | 0.1% | 0.5% | 5 | 3 | ||||||||

| Australian Unity | 1.0% | 0.8% | 8 | 3 | ||||||||

| BUPA | 31.3% | 2.5% | 8 | 6 | Yes | |||||||

| CBHS Corporate | 0.0% | 0.9% | 8 | 4 | ||||||||

| CDH | 0.0% | 0.5% | 8 | 8 | ||||||||

| CUA Health | 0.1% | 0.4% | 8 | 3 | ||||||||

| GMHBA | 0.9% | 0.9% | 5 | 4 | ||||||||

| HBF | 0.8% | 0.2% | 4 | 5 | ||||||||

| HCF | 5.5% | 1.0% | 8 | 6 | ||||||||

| HCI | 2.2% | 51.1% | 8 | 8 | Yes | |||||||

| Health.com.au | 0.2% | 0.7% | 8 | 3 | ||||||||

| Health Partners | 0.1% | 0.3% | 5 | 4 | ||||||||

| HIF | 0.2% | 0.6% | 8 | 4 | ||||||||

| Latrobe | 0.2% | 0.5% | 8 | 8 | ||||||||

| MDHF | 0.0% | 0.3% | 8 | 8 | ||||||||

| Medibank | 26.5% | 2.0% | 8 | 5 | Yes | |||||||